|

First

up – thank-you so very much to everyone who voted for us in

the China ii survey yesterday. Really appreciate it. If you haven’t

yet voted, we’d be grateful for your support for Real Estate – Karl Choi

& team + Corporate access; Helen Qiao in Economics & David Cui

in Strategy. Please

do let me know if you vote so we can say thank-you

2nd.

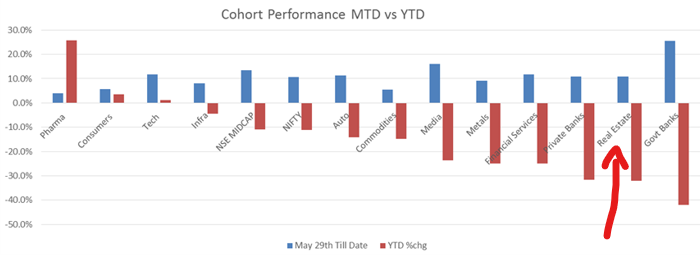

Focus is back on value stocks (vs gwth) which could

bode well for RE names (see note below from Savita). Investors are

showing a near record overweight in Gtowth. In that context, I thought

this chart from my colleagues in India (re Indian stocks) was

interesting

Source: Bloomberg

Headlines

l

Y’day:

NKY -0.87%, HSI -1.14%, SHCOMP -0.83%, KOSPI -0.11%

l

Overnight:

Dow +2.13%, SPX +1.34%, Nasdaq +0.94%

l

COVID: Moderna vaccine

è antibodies in all patients tested in initial safety trial, federal rschrs said

l

OIL: OPEC+ seeking extra production cuts from members that missed their tgts again in June

l

US: Trump issued an order to end HK’s special status w/ US

l

US: Trump signed HK bill which would sanction CN officials for cracking down political dissent

l

US: Re Phase 2, Trump "not interested right now in talking to China" b/c of virus pandemic

l

US: Reverses Student Visa Curbs After Harvard, MIT Fight

l

UK: Bans Huawei from 5G networks by ‘27; blocks new Huawei 5G equipment buys from end ‘20

l

CN:

Shenzhen rolls out property tightening measures… but mild – imposed on singles

l

CN: Regulators to move to avoid shadow banking resurgence. Concerns funds flowing into stock mkt

l

CN: 2 banks in East China have asked PBOC to ease capital adequacy rule, Reuters reports

l

CN: Spate of China Bank Runs Force Police, Regulators to Act (BBG)

l

CN: To lift ban on cross-province group tours

l

HK: DisneyLand announces temp closure due to increasing #of new COVID-19 cases.

l

HK: Emirates Airlines halts flights to & from HK

l

HK: Reports 48 new virus cases 14 Jul: 40 local. 24 w/ unknown sources of transmission

l

HK: Most short sold names y’day in HK incld Hysan (14, 64% of turnover) & Wharf REIC (1997, 44%)

l

JP: Tokyo to Raise Covid-19 Warning to Highest Lvl, Asahi Says

l

SG:`Very concerned' a/b 2nd virus wave: Chan

l

AU: VIC records 238 COVID cases in past 24hrs

Upcoming Conf calls:

l

Today: Navigating US volatility

& positioning, Jul 15, 8am HKT,

Registration.

l

Tomorrow:

Is Retail driving the mkt? Jul 16, 8am HKT,

Registration

l

Tomorrow:

Call w/ Woh Hup: Construction & prop devt outlook, Jul 16,

3:30pm HKT, Registration

l

Potential stamp duty

reform in Aust, July 22, 3pm Aus time, 1pm HKT/SGT.

Registration

Finally:

Walmart

is soon to unveil Walmart+, a $98/yr subscription plan that provides

members w/ a # of perks that will incl "same-day delivery of groceries

& general

merchandise, discs on fuel at Walmart gas stations, & early access

to product deals," according to multiple sources. The program seems to

be directly competing w/ Amazon Prime, which already offers many of the

same benefits. The fight over same-day grocery

delivery benefits b/w Walmart+ & Amazon Prime will largely be

fought by varying zip code demographics. Amazon acqd the upscale Whole

Foods in 2017, the locations of which are largely in urban & tonier

suburban areas. Walmart, on the other hand, is nearly

ubiquitous around the nation. 90% Americans live w/in 10 miles of a

Walmart, which presents a much larger mkt opportunity for Walmart+ for

subscription-based & same-day grocery delivery. (MSN)

|

|

Macro Rsch

|

|

|

US strategy:

Value vs Growth

(Savita Subramanian)

l

Val outperformed gwth in every size segment over the last century, but conspicuously stalled in ‘07

l

Will Val investing return?

7 reasons for a strong Value recovery, & 3 reasons that Gwth cld still lead.

|

|

|

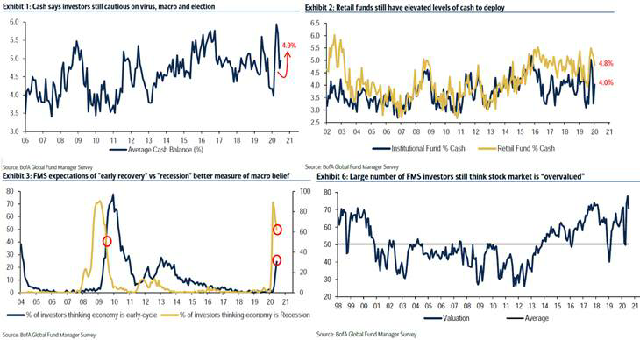

Global Fund Mngr Survey:

Investor

sentiment remains cautious (Michael Hartnett, Shirley Wu)

l

Consensus positioned for bad news on virus, macro, election

l

We say choppy/higher summer prices, sell SPX>3250, buy<2950.

l

Cash lvls

↑to

4.9% from 4.7%; Wall St's $24tn rally yet to elicit "greed";

l

BofA Bull & Bear Indicator is at 2.9, i.e. far away from worryingly bullish

lvls (>8.0).

l

74% say long

US tech stocks most "crowded trade" (highest reading in FMS history);

l

52% say COVID-19 2nd wave is largest "tail risk"; vaccine the catalyst to flip both.

l

72% xpct stronger global gwth, highest since Jan'14

l

Conviction in strength & duration of recovery low: 14% xpct "V", 44% "U", & 30% a "W".

|

|

China

|

|

|

|

Poly Devts (A):

Fundamentals

stabilize, but earnings gwth to slow ahead, Neutral, PO CNY17.80 (Karl, Van, Eric)

l

Sales recovery on track but still tgts flat contracted sales gwth in 2020.

l

Gross margin is likely to edge down to 28% nxt 3 yrs.

l

Plans to accelerate land acquisition in 2H20 given abundant cash on hand.

l

Maintain low financial costs & healthy net gearing.

l

Reiterate Neutral

|

|

|

China Merchants Shekou (A):

Surprisingly

negative 1H alert; maintain U/P, lower PO to CNY15

(Karl, Eric, Van)

l

Xpcts to post 1H net profit in range Rmb800m – Rmb1b, ~80% YoY

↓.

l

We project CMSK to record 20%+ gross profit margin in FY20E vs 25% in FY19 in A-sh basis.

l

Contracted sales on track (+15% YoY in 1H); proactive land banking so far (+120 YoY in 1H).

l

We further cut FY20E earnings by 9% & FY21/22E earnings by 5%.

l

Reiterate U/P,

cut PO to Rmb15 from Rmb16.

|

|

|

Equity:

Property-related loan growth capped; Bonds: Reit. UW CHJMAO'24/29 (Karl, Joyce)

l

PBoC continues capping growth in property-related loans.

l

Resi rent in Jun across 18 cities

↓3.2%MoM & 0.9%YoY, per Ke Rsch Institute.

l

Bond yld tightened 30bp to 9.02% WoW; Reit. UW CHJMAO ’24/29.

|

|

|

|

SZ rolls out 8 prop tightening measures.

Key points incl:

1) People can buy a home a/f getting SZ Hukou for 3yrs. 2) Improve

differentiated housing credit measures. 3) Adjusted VAT exemption period

for 2ndary housing from 2 yrs to 5 yrs. (JRJ)

>>> It is much milder than expected. Only imposed on singles & still large room for speculator to bypass.

China resumes inter-provincial team tourism,

per Ministry of Culture & Tourism. (The Paper)

At least 10 cities & provinces launched measures

to cool resi prop mkts in school districts. (CN Daily)

Sinic (2103HK) 1H contract sales Rmb43.5b,

completed 40% of FYr tgt. (Co)

Tahoe appointed financial advisor with regard to its debt restructuring

(the Paper)

CR Land: 1H rental fell 12% YoY

(announcement): But in June, investment properties of CRL recorded Rmb1.078b rental income,

YoY growth of 3.8%. June rental income performance slightly improved vs. May (+3.5% YoY).

5I5J (000560 SZ): negative earnings alert

(announcement) 5I5J, a secondary home agency in mainland China expects

to record Rmb30-40m net profit in 1H20, representing the YoY decline of 90%.

SZ Inv (604) 1H contract sales +17.8% on yr

Wheelock

puts 36 units in Ocean Marini resi project

up for sale this Sat, price HK$14,854-18,108/ft2. Co sold total 1615 units of Marini series projects for HK$14b since start of sales. (Co)

Px flat vs previous batch, but +14% vs 1st batch launched in early-March.

Henderson

Land sold a roof unit in Novum West resi project, Sai Ying Pun for HK$60.4m, or HK$48,000/ft2 (new high record in the project). Only 4 out of 645

units remain for sale. (HKET)

Landlords start to offer rental concessions a/f latest social-distancing measures

(HKET)

Bridgeway

Prime Shop Fund cut rent by 30% & purchased shopping coupons (to be

given out to consumers) for certain F&B street shop tenants. Laws

Group will offer rental concessions to F&B

tenants at D2 Place in Cheung Sha Wan in July, after having made such

concessions in Feb-Apr.

Citibank raises mortgage spread (Apple Daily)

A/f

moves by HSBC + BOCHK, Citibank raises mortgage rate from HIBOR+1.4% to

HIBOR+1.5% for mortgage loans below HK$6m. Prime rate cap remains

P-2.75%, or 2.5% currently.

Chow Tai Fok reports 72.5% SSS decline in June quarter (Apple Daily)

Down 72.5% YoY in HK; 93.2% YoY in Macau in June Q. China SSS fell 11.2%. Closed 3 shops in HK/Macau in the Q.

Eslite leased 8,000 sqf space at Sino Land’s Olympic City Three (HKET)

Former POPULAR bookstore space.

Singapore Economic Watch

Advance estimates showed 2Q GDP recording a historic drop of -41.2% qoq

SAAR, but this was not unexpected. We expect 2Q GDP to be revised

upwards subsequently once data for June, when the economy reopened, is

taken into account. We leave full-year f'cast at

-5.7%. Key risk is a return of lockdown measures, esp. with the recent

rise in community cases. (Mohamed Faiz Nagutha)

Singapore’s GDP

↓12.6%YoY in 2Q20, per Flash data. Worse than economists' xpctns of

↓10.5%, worse than 1Q's revised

↓0.3%. Fullyr f/c -7% ~ -4%. (Biz Times)

Guocoland

group CFO Lim Yoke Tuan resigns

a/f 2yrs at the job; no replacement named yet. (Co)

6-storey Genova Industrial Bldg + office

unit in Suntec City Twr 1 are up for sale w/ guide prices S$12m to S$13m, & S$2,900/ft2

respectively. (Biz Times)

2 corner shophouses in Lavender

for sale w/ S$13.2m guide price, freehold site 2,848ft2. (Biz Times)

Syd CBD apts vacancy moderated in Jun, 1st

↓since onset of pandemic; but asking rents also

↓sharply. (AFR)

Melb Hotel occupancy

↓53.4%YoY to 34% in Jun, per STR.

Hotel

demand in most Australian mkts unlikely to return to pre-COVID-19 lvl until 2023. (Hotel News Resource)

Qube sells Minto props in Syd’s south west to Charter

Hall entities for A$207m, initial yld 4.76%. (Co)

Ichigo Q1 (Mar 1-May 31) Rev

¥22.7b (↓13.5%YoY),

Op profit ¥3.65b (↓57%),

NI ¥2.2b (↓55%).

(Co)

Gurugaon devr M3M raised Rs5.7b ($76m)

from Oaktree Capital thru non-convertible debt. (VCCircle)

Oberoi Realty 1Q Net Income

Rs280.7m, ↓82%YoY.

Revenue Rs1.18b, ↓80%YoY.

Raising of Funds: approves raising Rs15b via debentures; raising up to Rs20b via equity sale. (Co)

Godrej hiked stake in Sobha from 1% to 9.99%

in March qrtr. (BQ) >> nb Kunal says this is the private family side, not Godrej props

Prestige Estates Unit buys stake in DB (BKC) Realtors. (BBG)

Malaysia’s retail industry

sales xpctd to ↓ 8.7%YoY in 2020,

per Retail Group Malaysia. (Star)

Govt

made no formal announcement on Metro Manila (NCR) lockdown status which

expires today. Those who are tasked to enforce quarantine rules believe

the NCR would most likely retain

its GCQ status & Cebu in ECQ. Govt with the help of the LGUs plan

to launch a house-to-house search for Covid19 patients they can transfer

to monitoring facilities.

Thailand Retail

The pandemic should have a negative impact on retailers' 2Q20 sales

& profitability. Sector SSSG should be -15% from the April-1H of May

lockdown. Post-lockdown, home improvement SSSG was strongest. (Sirichai

Chalokepunrat)

|

|

Rating

|

Price Objective

|

% chg to EPS

|

|

Stock

|

Curr.

|

Prev.

|

Curr.

|

%Chg

|

%↑↓side

|

2020

|

2021

|

2022

|

|

Poly Devs & Hldgs

|

N

|

|

17.80

|

8

|

5

|

|

|

|

|

CM Shekou

|

U

|

|

15.00

|

(6)

|

(21)

|

(9)

|

(10)

|

(10)

|

|

Weyerhaeuser Co

|

N

|

|

25.00

|

4

|

2

|

17

|

12

|

10

|

|

Rayonier Inc

|

U

|

|

31.00

|

3

|

19

|

50

|

|

|

|

PotlatchDeltic Corp

|

B

|

|

44.00

|

2

|

10

|

|

33

|

20

|

|

Investor Invites

|

|

Navigating US volatility & positioning, 8am HKT

|

RSVP

|

HK – conf call

|

Jul 15

|

|

Is Retail driving the mkt? 8am HKT

|

RSVP

|

HK – conf call

|

Jul 16

|

|

Stamp duty reform in Aust, 1pm HKT

|

RSVP

|

HK – conf call

|

Jul 22

|

|

Vonovia video calls, 2pm, 3pm, 4pm, 5pm HKT

|

RSVP

|

HK

|

Aug 25-28

|

|

Vonovia video calls, 2pm, 3pm, 4pm, 5pm CST

|

RSVP

|

Taiwan

|

Aug 25-28

|

|

|

|

|

|

|

Stamp duty reform in Aust, 1pm SGT

|

RSVP

|

SG– conf call

|

Jul 22

|

|

Vonovia video calls, 2pm, 3pm, 4pm, 5pm SGT

|

RSVP

|

SG

|

Aug 25-28

|

|

Vonovia video calls, 2pm, 3pm, 4pm, 5pm MYT

|

RSVP

|

Malaysia

|

Aug 25-28

|

|

|

|

|

|

|

Stamp duty reform in Aust, 3pm AUT

|

RSVP

|

AU– conf call

|

Jul 22

|

|

Vonovia video calls, 4pm, 5pm AEST

|

RSVP

|

Aust

|

Aug 25-28

|

|

|

|

|

|

|

Mitsubishi Estate, 3pm HKT / 4pm JST / 8am BST

|

RSVP

|

Asia/EMEA

|

Aug 14

|

|

Mitsubishi Estate, Aug 26 8am HKT / 9am JST / Aug 25 8pm EST

|

RSVP

|

Asia/US

|

Aug 26/25

|

|

Vonovia video calls, 3pm, 4pm KST

|

RSVP

|

Korea

|

Aug 25-28

|

|

Vonovia video calls, 3pm, 4pm JST

|

RSVP

|

Japan

|

Aug 25-28

|

|

|

|

|

|

|

2020 Japan Conference

|

RSVP

|

Tokyo

|

Sep 7-11

|

|

Global Real Estate conference 2020

|

RSVP

|

NYC

|

Sept 15 -16

|

|

|

|

|

|

|

Clients can access our

always up-to-date Global Property val database here

* My pa holdings: BAC US, 1 HK, 6 HK, ST SP

|